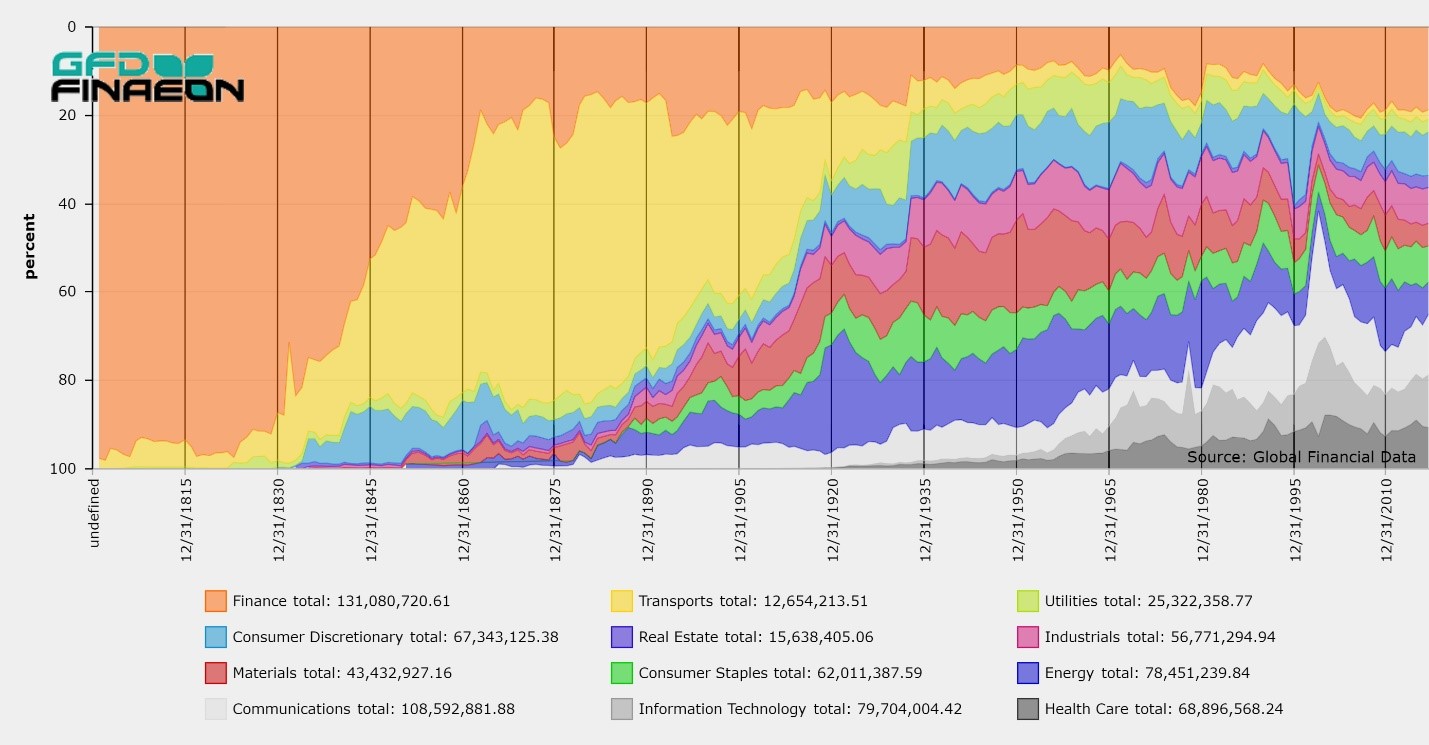

The Company of Proprietors of the Grand Junction Canal was incorporated by Special Act of Parliament on April 30, 1793 to build a canal from Braunston to the River Thames. The stock for the canal went through three bubbles, in the 1790s, the 1810s and the 1820s, before settling down once the railroads were built, providing competition to the canal.

Unfortunately, there is almost no data for the Canal Mania of the 1790s. The number of canals authorized by Act of Parliament in 1790 was one, but by 1793 twenty were authorized. The capital authorized in 1790 was £90,000, but had risen to £2,824,700 by 1793. Most of the canals raised their money locally, mainly in the Midlands, and there were few transactions in the stocks as a result. Though a stock exchange was established in Liverpool to trade shares, actual values are hard to come by and must be tracked down through newspapers. Nevertheless, some of the stock increases were impressive. The Birmingham and Fazeley showed the greatest increase, trading at a premium of £1170 in 1793.

The first bubble occurred in 1792 and 1793 and we only have two prices for Grand Junction Canal Shares, one at £472.75 in October 1792, a premium of 355 guineas, even before the company had started to dig the canal or gotten approval from Parliament! Talk about a speculative bubble. Shares had fallen to £441 by the time the approval was provided by Parliament, and the prices collapsed after 1795 when shares returned to their par level of around 100.

The London Stock Exchange wasn’t formally established until 1801, so until then the opportunity to trade canal stocks and keep track of the price fluctuations was limited. Even once the London Stock Exchange was established in 1801, most of the prices we have from the Gentlemen’s Magazine and other sources. The data are bid and ask quotes rather than actual prices since the shares still traded infrequently. Nevertheless, these data are sufficient to outline the three bubbles in shares of the Grand Junction Canal. The next price we have for Grand Junction Canal shares after 1793 is of £94 in April 1806. The bubble began in May 1808 when the shares still traded at £96, but the price steadily rose to £313.5 by June 1808, whence they declined to £179 by August 1811, stabilized around 200 until 1815 when the Napoleonic War ended, then fell to £103 by September 1816. The second Canal Mania of the 1810s was not as wild as the one of the 1790s, since share prices tripled rather than quadrupled, but the difference was that the Canal Mania of the 1810s was not limited to the Midlands. Shareholders in London also participated as a result of the establishment of the Stock Exchange.

The London Stock Exchange wasn’t formally established until 1801, so until then the opportunity to trade canal stocks and keep track of the price fluctuations was limited. Even once the London Stock Exchange was established in 1801, most of the prices we have from the Gentlemen’s Magazine and other sources. The data are bid and ask quotes rather than actual prices since the shares still traded infrequently. Nevertheless, these data are sufficient to outline the three bubbles in shares of the Grand Junction Canal.

The next price we have for Grand Junction Canal shares after 1793 is of £94 in April 1806. The bubble began in May 1808 when the shares still traded at £96, but the price steadily rose to £313.5 by June 1808, whence they declined to £179 by August 1811, stabilized around 200 until 1815 when the Napoleonic War ended, then fell to £103 by September 1816. The second Canal Mania of the 1810s was not as wild as the one of the 1790s, since share prices tripled rather than quadrupled, but the difference was that the Canal Mania of the 1810s was not limited to the Midlands. Shareholders in London also participated as a result of the establishment of the Stock Exchange.

The next move up in the shares began soon after the post-war plummet. Shares moved up steadily from September 1816 to hit £200 by the end of 1817, stabilized around £200 through the end of 1820, then hit £383 by April 1824. The canal stocks shared in the bubble of the 1820s even though that bubble mainly revolved around South American stocks and the mining companies that were established following the independence of the South American countries.

Unfortunately, Grand Junction Canal shares did not benefit from the railway mania of the 1840s since the railways were in direct competition with the canals and shareholders sold their canal shares to invest in railways. Shares traded steadily between £200 and £300 between 1825 and 1845, but fell along with the Railway Mania crash, with shares falling to £51 by 1853.

Shares generally rose for the rest of the nineteenth century, hitting £150 in 1897 before declining until the 1920s bull market. The Regent’s Canal bought the Grand Junction Canal and the three Warwick canals, and from January 1, 1929 they became part of the (new) Grand Union Canal. The Grand Junction Canal took the proceeds and became a REIT which was renamed the Grand Junction Co., Ltd. The company was acquired by the Amalgamated Investment & Property Co. Ltd. in 1971.

Bubbles require both a source for the speculation, a new technology that excites investors and causes cash to quickly flow into the new discovery, and excess credit being made available to invest in the shares. The initial canal mania was driven by profits with one canal paying a £75 dividend. Many of the stocks were profitable, and did quite well, but others that were poorly thought out failed. The two bubbles that drove Grand Junction Canal shares in the 1810s and 1820s were driven not only by the investment opportunities the canals provided, but by the liquidity created by the impact of the Napoleonic Wars on Britain finances.

Between 1793 and 1818, the UK government debt rose from £243 million to £843 million in 1818. The brief hiatus in the increase in debt between 1808 and 1812 could help to explain the canal mania of 1810-1812 as the Continental Blockade forced investors to put their money to work internally, but once Napoleon invaded Russia, the source of funding dried up. 1819 was when the UK government debt peaked at £844 million, declining from there in absolute terms, much less as a share of GDP, until 1914.

It should be remembered that more than anything else, Napoleon made London the financial center of the world. The French Revolution both destroyed the rich in France through driving wealthy financiers out of Paris and to London, and through inflation, which destroyed the value of the assets the rich had held. The other financial center in the eighteenth century in Europe was Amsterdam, but it never really recovered from the occupation of French troops in 1795. Both financial expertise and capital flowed to London as a result of the French Revolution and the wars that followed, and the laissez-faire approach England took to markets ensured that London would be the financial center of the world until World War I.

As capital flowed into London during and after the Napoleonic Wars, and investors were allowed to trade freely, stocks benefited. Anyone who questions the impact of the government on the price of financial assets, both positively and negatively, need only look at the Grand Junction Canal’s history as well as that of the London stock exchange to see the impact the government can have.