Bryan Taylor, Chief Economist, Global Financial Data

Global Financial Data has made major revisions to three of its popular indices, the Dow Jones Transport Average, the S&P 500 Composite and the S&P 500 Composite Total Return Index.

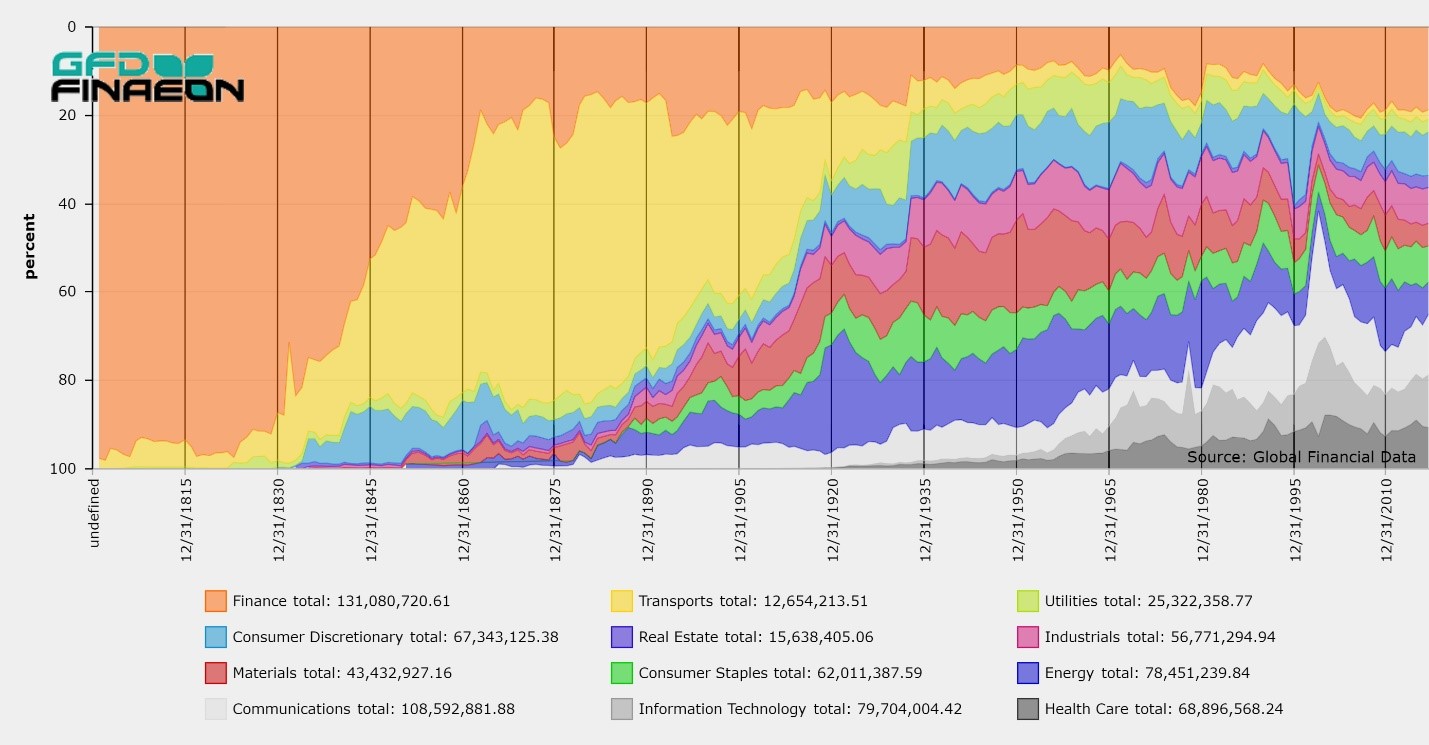

Global Financial Data has recently calculated its own GFD Index for Railroad stocks in the 1800s. Using data GFD has collected on the price of shares, dividends paid on shares and the number of shares outstanding, GFD has calculated a cap-weighted index of the price and total return to railroad shares from 1832 until 2018. In each year, Global Financial Data chose the top 40 companies by capitalization, then narrowed the list down to the top 25 companies by liquidity and used those 25 companies to calculate GFD’s Railroad Index. The index is illustrated below.

GFD Railroad Index, 1832 to 1899

We have appended the data for the GFD Railroad Index to the Dow Jones Transportation Average to provide a GFD Extension back to February 3, 1832. This provides the index with 57 additional years of daily history since the Dow Jones Railroad Index was introduced on September 23, 1889.

For the S&P 500 Index, we had previously used data from Smith and Cole from 1834 to 1862 and from Macaulay from 1863 to 1870. Data from the Cowles Commission is used beginning in 1871. The data from Smith and Cole and from Macaulay were calculated as an equal-weighted index in the 1930s using a more limited number of securities. Also, their data were unable to use dividends to calculate total returns for their index. The GFD Indices are cap-weighted rather than equal-weighted and include dividends to calculate total returns. Consequently, the GFD Indices are superior to the Smith and Cole and Macaulay indices and will be used to extend the S&P 500 between 1834 and 1870.

The Smith and Cole and Macaulay indices were equal-weighted while the GFD Indices are capitalization-weighted. As has been documented, equal-weighted indices tend to provide a higher return than capitalization-weighted indices because of the small-firm effect. That happened in this case. The equal-weighted data from Smith and Cole and Macaulay had an annual price return of 2.81% between 1834 and 1870 while the GFD Cap-weighted index had an annual return of 1.41% during the same period of time.

We had previously assumed that the dividend yield on the railroad stocks was equal to the yield on U.S. government bonds plus 1%, implying a 1% equity risk premium. The average yield on U.S. government bonds between 1833 and 1870 was 4.53% per annum giving an assumed average yield of 5.53%. However, the actual dividend yield on railroad stocks during this period of time was 5.82% and the total return to railroad stocks was 7.32% per annum. The price return for the old index was 2.81% and the imputed dividend yield was 5.53% producing an overall total return to the old index of 8.05%.

We feel that the new index data provides a more accurate measurement of the total return to stocks in the United States between 1834 and 1870. Therefore, we have replaced the old Smith and Cole and Macaulay data with GFD’s more accurate calculations.

Global Financial Data is currently working on calculating indices for the banks, insurance companies and other corporations that were listed in the United States in the 1800s and hopes to add this data to the indices later this year.

We encourage subscribers to download the corrected data. If you currently do not have access to this data, please feel free to call Global Financial Data today to speak to one of our sales representatives at 877-DATA-999 or 949-542-4200.

REQUEST A DEMO with a GFDFinaeon Specialist

Information

Our comprehensive financial databases span global markets offering data never compiled into an electronic format. We create and generate our own proprietary data series while we continue to investigate new sources and extend existing series whenever possible. GFD supports full data transparency to enable our users to verify financial data points, tracing them back to the original source documents. GFD is the original supplier of complete historical data.

Global Financial Data has made major revisions to three of its popular indices, the Dow Jones Transport Average, the S&P 500 Composite and the S&P 500 Composite Total Return Index.

Global Financial Data has recently calculated its own GFD Index for Railroad stocks in the 1800s. Using data GFD has collected on the price of shares, dividends paid on shares and the number of shares outstanding, GFD has calculated a cap-weighted index of the price and total return to railroad shares from 1832 until 2018. In each year, Global Financial Data chose the top 40 companies by capitalization, then narrowed the list down to the top 25 companies by liquidity and used those 25 companies to calculate GFD’s Railroad Index. The index is illustrated below.

Global Financial Data has made major revisions to three of its popular indices, the Dow Jones Transport Average, the S&P 500 Composite and the S&P 500 Composite Total Return Index.

Global Financial Data has recently calculated its own GFD Index for Railroad stocks in the 1800s. Using data GFD has collected on the price of shares, dividends paid on shares and the number of shares outstanding, GFD has calculated a cap-weighted index of the price and total return to railroad shares from 1832 until 2018. In each year, Global Financial Data chose the top 40 companies by capitalization, then narrowed the list down to the top 25 companies by liquidity and used those 25 companies to calculate GFD’s Railroad Index. The index is illustrated below.