Global Financial Data has calculated the market cap of the United States stock market from 1791 until 2018. These calculations include not only the New York Stock Exchange, American Stock Exchange and NASDAQ, but regional exchanges, such as Philadelphia and Boston and over-the-counter stocks, such as Standard Oil. We have divided the total market cap by GDP to examine how the stock market has grown relative to the economy over the past 200 years.

The graph below illustrates the results. There were two periods when there was a dramatic increase in the ratio of market capitalization to GDP over the past two hundred years. Both of these shifts occurred during communication revolutions which enabled the market to both build the infrastructure for these changes and enabled investors to have greater access to the stock market. In both cases, the communication revolutions that occurred encouraged globalization and the growth of the stock market.

Given this, we break down the growth of the stock market into four periods:

- Antebellum America (1791-1865) in which the stock market grew with the economy and the market cap/GDP ratio stayed around 10%,

- Globalization (1865-1914) during which the United States raised capital from Europe to help build its economy and the market cap/GDP ratio rose from 10% to 50%. During this period of time the telegraph and telephone linked the world’s stock exchanges together creating a global market for shares,

- Regulation (1914-1980) during which the market cap/GDP ratio fluctuated around 50% as regulation, war, inflation and nationalization constrained the growth in the market cap/GDP ratio, and

- Deregulation (1980-2018) in which the market cap/GDP ratio grew to over 100% of the economy. The introduction of computers and the internet enabled traders to reduce the time a trade could take place from minutes to nanoseconds and enabled the stock exchange to move from a trading floor to computers

Although these four periods are not generally recognized as parameters that can be used to analyze changes in American financial markets, we feel they should be. In each case, the government’s attitude toward corporations changed, allowing the market cap of listed corporations to grow or remain constant relative to the rest of the economy. Other factors such as war, inflation, nationalization and regulation also influenced this ratio. The final change occurred at the end of the twentieth century, deregulating the financial sector which produced a shift upward in the market cap/GDP ratio to over 100%.

Data Sources

Global Financial Data has collected data on 50,000 securities that have traded in the United States over the past 225 years. GFD has data on the prices of stocks, the dividends and corporate actions, and the shares outstanding for each company. By multiplying the market price of each stock times the number of shares outstanding, we can calculate the market cap for each company, and by summing these numbers, we can calculate the total market capitalization for the United States.

Our data set is limited to companies that operated in the United States. Companies that operated sugar plantations in Cuba before 1959, for example, are excluded as are American Depository Receipts (ADRs) and other foreign corporations. Although the number of foreign companies that listed in the United States was almost non-existent in the nineteenth century, the number grew rapidly during the twentieth century and today thousands of ADRs trade on U.S. exchanges. The market cap data we have collected only includes American companies.

We took the calculations of GDP for the United States from the Bureau of Economic Analysis to determine how the ratio of market capitalization to GDP has changed over time. The result is provided in the graph below. A value of 100 means that the stock market capitalization was equal to 100% of GDP.

United States Market Capitalization as a Share of GDP, 1791 to 2018

Three major shifts in the ratio of market cap/GDP are readily apparent. The first occurred after the Civil War when international capital flowed into the United States to fund the growth of railroads, communications and other industries. The telegraph connected American cities in the 1840s and in 1866, a transatlantic cable linked New York to London and the rest of Europe. By the end of the century, the telephone began displacing the telegraph.

The market cap/GDP ratio more than tripled from around 15% in the 1860s to 50% by the 1900s. During this period of time many industries amalgamated into Trusts that attempted to run their industry as a monopoly. Antitrust laws and other regulations put an end to these shifts. When World War I began, regulation, inflation and war kept the market cap/GDP ratio from growing. Between 1915 and 1980, the ratio fluctuated up and down, hitting a high during the bull market of the 1920s and the economic growth of the 1950s and 1960s, and reaching low points after World War I and World War II.

There are several reasons why regulation, inflation and war limit growth in the market cap/GDP ratio. Government regulations can restrict corporations from growing in size or limit corporations’ ability to issue new capital.

Higher rates of inflation discount the present value of future corporate cash flows. The bouts of inflation in the United States that occurred after World War I, World War II and the Vietnam War clearly drove the market cap/GDP ratio down. War affects the ratio both indirectly through higher inflation and directly because resources are reallocated from funding the growth of new companies to funding the war. New issues of securities are discouraged by the government so resources can be reallocated to pay for the war.

During the 1980s, a third shift in the market cap/GDP ratio occurred when the ratio more than doubled, increasing from around 50% in the early 1980s to over 100% by the end of the 1990s. The introduction of computers and the internet made the old trading floor obsolete. Traders could place their orders online and the orders were filled in nanoseconds. The Reagan administration deregulated the economy and shifted the regulatory burden of proof on the government, not on corporations.

With the exception of the financial crisis of 2008, the market cap/GDP ratio has stayed above 100% during the past 20 years. We argue that as a result of this second communications revolution, the increase in the market cap/GDP ratio over 100% is a permanent shift that will probably keep the ratio above 100% for the rest of the century.

Antebellum America

It is surprising that the market cap of United States stayed around 10% consistently from 1791 until the 1860s despite the rapid changes in the American economy. However, it is important to differentiate between growth in the American economy and changes in the capitalization of corporations in the United States. Although the market cap of the stock market grew in line with the economy before the civil war, its growth did not exceed that of the economy until after the Civil War.

When the Bank of the United States was capitalized at $10 million in 1791, the GDP of the United States was only $200 million and the market cap of the three banks and one industrial firm that were listed totaled $17 million.

Initially, virtually all the companies that listed in New York, Philadelphia, Boston or other exchanges were in insurance or banking, but gradually other industries appeared. Transport stocks started trading in 1801. First there were turnpikes, most of which were too small to trade on the exchanges, then there were canals which did trade on exchanges and in the 1830s, railroads made their appearance.

Railroads dominated the stock market of the United States throughout the 1800s. Utilities started trading in 1804, and in the 1830s, hundreds of mills were established in Massachusetts producing textiles and clothing for the country. The mills traded primarily on the Boston stock exchange, and by the 1840s, these mills represented over 10% of U.S. stock market capitalization. Over the next couple decades, energy companies started producing coal, industrial manufacturers appeared, mining companies started mining for copper, silver and gold, and the first real estate companies issued shares.

Despite all of these changes, the stock market could barely keep up with the growing American economy. Between 1791 and 1861, the market cap of the United States grew twentyfold, from $17 million to $345 million, but America’s GDP grew at a similar pace, increasing from $200 million to $4 billion. Then the Civil War changed the American economy forever.

The Gilded Age and Globalization

Once the Civil War was over, the pace of growth in the United States and the stock market quickened dramatically. Between 1865 and 1901, the American economy grew from $6 billion to $20 billion, but the market cap of companies listed in the United States grew from $635 million to over $10 billion. The ratio of stock market cap to GDP grew from 10% to over 50% as hundreds of companies raised capital by issuing shares. Once the war was over, the robber barons of the gilded age built the railroads, steel and other industries that built America.

The telegraph enabled traders in different American cities to connect directly with brokers at the stock exchange, and the telephone enabled investors to speak directly to brokers in New York. By 1866, a transatlantic cable had been laid, linking the American and European continents. By the end of the century, a global system of telecommunications connected all the stock exchanges of the world together, laying the foundations for the globalization of international finance.

Not only did this communications revolution enable investors to buy and sell stocks more, but corporations had to raise the capital to fund the growth in America’s infrastructure. This combination of factors pushed the market capitalization of companies listed on the stock exchanges to half of GDP by the end of the century.

The period from 1865 to 1914 was the height of globalization. Railroads in the United States took advantage of this and marketed their stocks and bonds in London, Amsterdam, Paris, Berlin and other European stock exchanges. The United States raised huge amounts of capital and in the process became a net debtor to the rest of the world, but in the process, it was able to build the infrastructure for the American economy. Railroads raised over one-third of their capital in Europe.

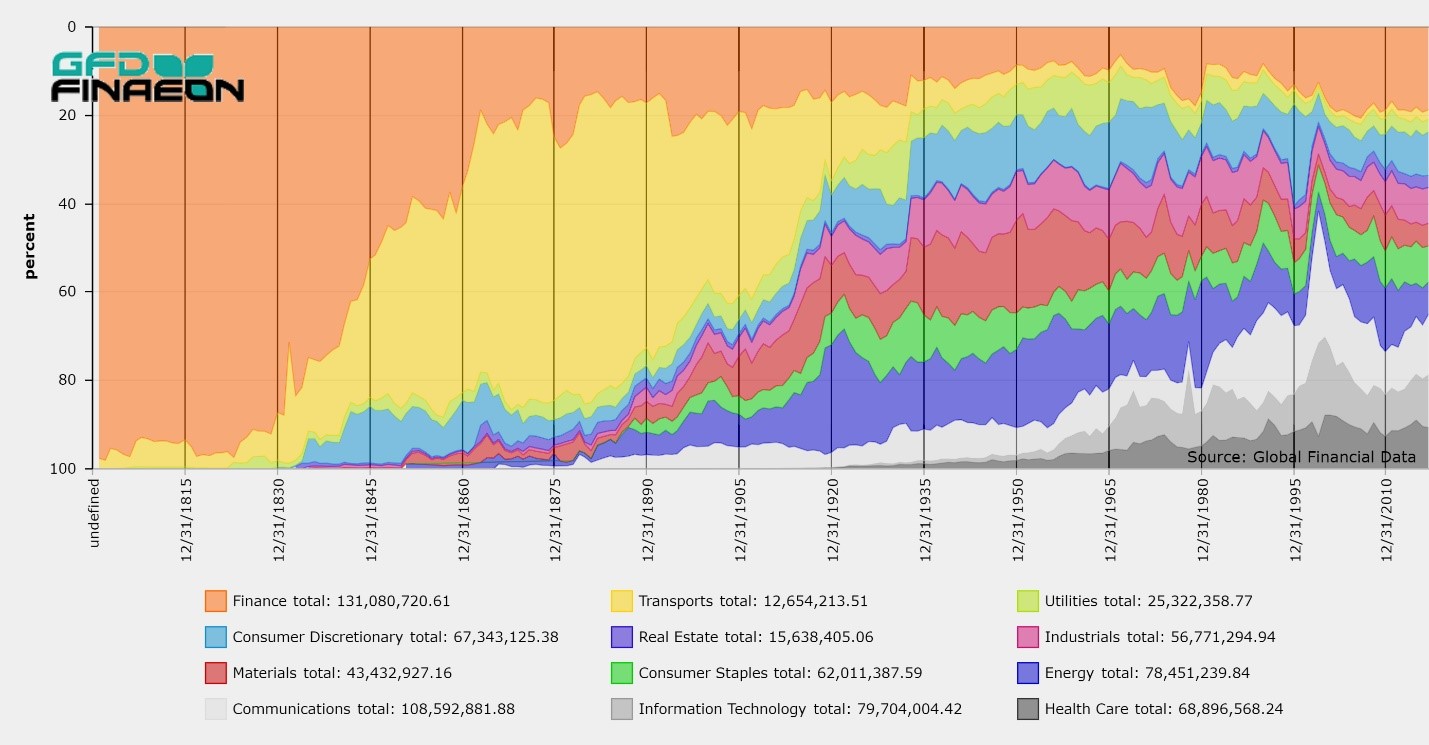

As was true in antebellum America, the American economy underwent rapid changes after the Civil War. The chart below illustrates how the sectoral composition of the American stock market changed over the past 200 years. Although the largest share of market capitalization in the 1800s was concentrated in the railroads, their share shrank between 1865 and 1914, Other sectors, especially energy and industrials grew even more dramatically than railroads with Standard Oil, AT&T and U.S. Steel becoming some of the biggest companies in the world.

Sectoral Allocations in the United States, 1800 to 2018

Between 1865 and 1901 railroads shrank from 58% of the total market cap to 40%, finance shrank slightly from 23% to 19%, but the real growth was in materials and energy. In 1865 the Illinois Central Railroad was the largest company in the United States, but in 1901 Standard Oil was over twice the size of the next largest company, Penn Central.

The third largest sector by market cap in 1865 was consumer discretionary, primarily made up of the mills in New England, but in 1901, communications, consumer staples, energy, industrials, materials and utilities were all larger than consumer discretionary. In 1901, energy was the third largest sector in the United States, having grown from 2% in 1865 to 10% by 1901. Even more impressive was the growth in Communications. There were no communications companies listed in the United States in 1861, but between the telegraph and telephone, communications grew to almost 6% of the total market cap in the United States by 1901.

The leaders of industry in the last third of the 1800s played an essential role in converting corporations into capital that could be owned by investors. By the end of the nineteenth century, the Gilded Age was over and the era of trusts in which industries amalgamated to create single companies that oversaw the production of oil, cigarettes, sugar and other goods dominated the economy. Without the conversion of companies into shares that could be bought and sold, the conversion of the economy into a collection of industrial trusts would not have been possible.

Government Regulation

Globalization came to an end on July 31, 1914 when the world’s stock exchanges closed down at the beginning of World War I. The U.S., U.K. and French stock markets reopened by the end of 1914, but the German and Russian stock markets didn’t reopen until 1917. When the October Revolution began in Russia, the St. Petersburg bourse closed for the next 75 years.

The period between 1914 and 1980 was one of financial repression in which government regulation of financial markets and the economy prevented the stock market from increasing its share of GDP. There were periods such as the 1920s, 1950s and 1960s in which financial markets operated relatively freely and grew, but there were also periods of regulation (1930s), inflation (1920s and 1970s) and war (1910s, 1940s, 1970s) during which market cap’s share of GDP declined.

When the United States entered World War I, capital shifted from investing in new companies to funding the war, and the flow of capital from Europe to America came to an abrupt halt. After the war, one of the primary enemies of investors raised its head: inflation. Although inflation has never wiped out American investors as it did in Germany during the 1920s, inflation has reduced the return to investors and shrank the market cap/GDP ratio in the 1920s, 1940s and 1970s.

Inflation is the greatest enemy of investors. Higher inflation leads to higher interest rates which reduces the price of bonds. High inflation also means lower stock prices. The value of a company depends upon the discounted value of future cash flows. As inflation rises, interest rates increase and the discounted value of future cash flows declines causing stock prices to decrease. When inflation increases, as it did after World War I and in the 1970s, the market cap/GDP ratio declines. Whenever, disinflation occurs, as it did in the 1920s and after 1981, the market cap/GDP ratio rises.

The 1920s, of course, led to a bull market that is still remembered, and by the summer of 1929, for the first time in its history, the market cap of all stocks listed in the United States exceeded national GDP. In September 1929, the market cap of stocks listed in the United States reached $125 billion while nominal GDP was at $106 billion. Although GDP fell to $60 billion by 1932, the stock market cap fell to $25 billion. Market cap did not exceed GDP again until the 1990s when a new communications revolution, the dotcom bubble, deregulation and disinflation drove this ratio to the highest level it has ever been.

Once the United States entered World War II in 1939, capital was directed toward the war effort and the market cap/GDP ratio fell to 23% during the war. Even as late as 1948 the market Cap/GDP ratio was under 25%, but in 1948 as the cold war broke out, and the United States focused on growing the economy once again, the ratio began to rise.

Growth in the stock market affected all the sectors in the economy. In 1968, the market cap/GDP ratio reached 87%, the highest it had been since 1929. The Nifty Fifty became the benchmark for the stock market and just as it looked like the market cap would exceed GDP, OPEC upended the market. The price of oil went from $3 in 1972 to $39 by 1982 and stagflation became the dominant theme of the economy.

Interest rates had been slowly rising since the 1940s until they reached double digits in 1982. Since the value of companies depends upon the discounted value of future cash flows, stock prices were hit badly, and the market cap/GDP ratio fell from 87% in 1968 to 37% in 1974. As in most cases in stock market history, when things looked the darkest, it was the best point to invest.

Deregulation

Ronald Reagan was elected president in 1980 and he deregulated the economy to promote economic growth. At the same time, Paul Volcker fought inflation and initiated the beginning of a 35-year decline in interest rates. Moreover, technology in the form of computers, the internet and biotechs began to dominate the stock market as a new communications revolution began. The yield on the 10-year bond fell from over 15% to under 5% between 1981 and 1999. The market cap/GDP ratio rose from 38% in 1981 to 163% in 1999 more than quadrupling the ratio. All the stars were aligned to move capital into the stock market.

Once again, a communications revolution broke over the stock market. Computers enabled trading times to shrink from minutes to nanoseconds. The internet enabled investors to place trades directly with the stock exchange without having to use a human broker. Information technology and communication stocks grew in size rapidly and contributed to the growth in the size of the market. It was in large part because of this communications revolution that the financial world became globalized once again.

Deregulation became a world-wide phenomenon. Margaret Thatcher and Ronald Reagan promoted the growth of the economy through deregulation. The Big Bang opened up financial markets in London. The Berlin Wall and the Soviet Union fell. The four Asian tigers (Japan, Taiwan, Korea and Singapore) were able to achieve rapid growth through exports and both China and Russia opened up stock markets in formerly communist countries. The global market cap/GDP ratio rose from around 25% in 1980 to over 100% by 2000, mirroring the trend in the United States as is illustrated below.

Global Market Capitalization as a Share of GDP, 1900 to 2018

Deregulation, falling interest rates, disinflation and rapid growth created a stock market bubble in 1999 and a financial crisis in 2008. The dotcom bubble was one of the primary factors driving growth in the economy and in the stock market. The market cap of information technology grew from only $200 billion in 1990 to over $4.5 trillion by 1999. The market cap of the entire U.S. stock market in 1990 was only $2.8 trillion. With the growth of the internet, products went global. By 2018, a website like Facebook had over 2 billion active monthly users, bringing over 25% of the global population together on a single website.

Nevertheless, the financial crises of the twenty-first century have created a rollercoaster ride. The dotcom bubble burst in 2000. September 11 and other market crises, such as the bankruptcy of Enron and Worldcom, caused the market to lose almost half of its market cap. The market bounced back during the growth engendered by the attempt to convert mortgages into tradable capital, but the financial crisis of 2008 and the Great Recession that followed caused the market to lose half of its capitalization, briefly pushing the market cap/GDP ratio below 100%. Since then, the market has bounced back, and now this ratio is pushing back toward the highs of 1999.

The Future of the Stock Market

Where do we go from here? Will the market cap/GDP ratio reach 200% in the near future, or will it fall back below 100% in the next financial crisis? Although we can’t answer that question, it does appear that the deregulation and disinflation at the end of the twentieth century has permanently pushed the market cap/GDP ratio in the United States above 100% and it is likely to stay above that ratio for decades to come. The current communications revolution is not over and will continue to transform the economy and the financial sector.

However, there is no guarantee the market cap/GDP ratio will stay above 100%. One question this survey raises is what would have happened if World War I had not begun in 1914? Would globalization have continued and the 70 years of financial repression and inflation which held back the growth of the market cap/GDP ratio not have occurred? The great reversal in the growth of the market cap/GDP ratio was a global phenomenon, not just an American phenomenon as the global capitalization/GDP graph above shows.

The rise of nationalism in politics in the United States, United Kingdom, Russia and China certainly makes one wonder how much longer the growth in market cap can continue to grow relative to GDP. With interest rates close to zero in Europe, Japan and the United States, disinflation is more likely to reverse than continue. The other two nemeses of the market cap/GDP ratio, war and regulation are less predictable. Although war is unlikely, it also seemed unlikely in 1913 when the 70 years of financial repression began. The biggest threat today is probably that nationalism could lead to trade wars which could threaten economic growth.

This article shows how the cost of inflation, regulation, war and nationalism over the past 200 years constrained the growth in the market cap/GDP ratio while deregulation, communication revolutions and globalization helped it grow. The optimal situation is one of globalization and low inflation with minimal regulation of financial markets; however, a lack of regulation also generates periodic financial crisis leading to reregulation.

Let us hope we have learned the lessons of the past 200 years and that the growth of financial markets can continue in the decades to come.